S Corp filing: Tax information small business owners need to know

Key Takeaways

- S Corporation status can have tax advantages, including pass‑through taxation and reduced self‑employment tax, making it a popular choice for small business owners looking to maximize tax savings.

- S Corp owners must pay themselves a “reasonable salary”—that is, a salary in line with their responsibilities with the company and industry benchmarks.

- S Corporations must meet ongoing tax filing requirements, including filing Form 1120‑S annually, sending Schedule K‑1s to shareholders, and following any state‑specific S Corp filing obligations.

If you’ve ever wondered how to start an S Corp, look no further. S Corp tax benefits can be substantial, so business owners should know about the S Corp business structure and advantages of becoming an S Corporation. This guide will walk future S Corporation owners through S Corp filing information and three steps for creating an S Corp.

What is an S Corporation?

An S Corporation, or S Corp, is a tax election that allows a business to qualify for special pass-through taxation status. If you’re a new business owner, distinguishing between S Corp, C Corp, and Limited Liability Company (LLC) can be confusing. The critical thing to know is that an S Corp is not a business structure. It’s a tax status, or election, with its own set of advantages and restrictions for tax purposes. Both LLCs and corporations can complete the S Corp election process. Most U.S.-based entities can apply for S Corp status if they meet S Corp shareholder requirements.

S Corporation shareholder requirements include having no more than 100 S Corp shareholders, who all must be individual US citizens. Additionally, the S Corp can only have one class of stock, and certain types of businesses, such as financial institutions and insurance companies, are ineligible.

What structure is right for my business?

Answer these six questions to help you find your fit

Advantages of becoming an S Corp

Why would you want your small business to take an S Corporation election? There are a few advantages.

The primary benefit of starting an S Corp is that business revenue becomes eligible for pass-through taxation. Another plus is that the business’s profits are not subject to self-employment taxes. The difference in self-employment taxes an owner pays when filing taxes as an S Corp vs. LLC can be substantial.

Looking for another upside? How about this: Once the IRS approves a business’s S Corp filing, the S Corp owner can begin paying themselves a reasonable salary. It’s important to note that a “reasonable salary” is defined on a case-by-case basis and should reflect the value of the work completed by the owner. Generally, a reasonable salary is about 40%-60% of company profits for a business with a single owner and no employees.

How to start an S Corp

Step One: Form an Entity

The first step in creating an S Corp is to create an entity (if you haven’t already). You can create an entity by registering your business in your state as an LLC or a corporation. You can file the paperwork yourself or hire a third party, like Block Advisors, to assist you in creating and filing appropriate S Corporation status paperwork.

Step Two: Get an Employer Identification Number (EIN)

If your business doesn’t already have an EIN or is required to get a new one, you should file an Internal Revenue Service (IRS) Tax Form SS-4 to apply for an EIN. Find out more about getting an EIN.

If you choose to form a new entity with Block Advisors, all our packages include an EIN application, making it easy to check one more thing off your list.

Step Three: Filing the S Election

To create an S Corp, your business must make an S election by mailing or faxing IRS Form 2553 to the IRS by the S Corp filing deadline. If you have an established business entity and are just learning about S Corp tax implications, you may still be able to change your election. Read Form 2553 late filing: Making up for lost time on S Corp elections to learn more about late election relief.

It’s ok if this part of the S Corp filing process feels intimidating. Whether you are starting a new business or converting an existing business to an S Corp, Block Advisors can take the paperwork off your hands to relieve some of the stress of your S Corp filing requirement.

Note: Your operating agreement and/or bylaws, depending on whether you formed an LLC or corporation at the state level, should state you wish to be taxed as an S corp. These documents should also specify that distributions are based solely on ownership percentage. If you don’t have this language currently worked into your operating agreement or bylaws, you must amend them to include these statements. Even if you are a single-member LLC, it is still a good idea to include these statements in case you decide to add a new member-owner.

Find out if an S Corp election is right for you

See if you could be saving thousands at tax time.

Annual S Corp Tax Filing Requirements and IRS Tax Forms

S Corporations must file a business tax return with the IRS each tax year. IRS Form 1120S must be completed and submitted by the business tax deadline each year—usually March 15th for calendar year tax filers. Following the tax return, S Corporations must provide each shareholder with a Schedule K-1 form, allowing them to report S Corporation income on their personal tax returns. You must also complete quarterly tax filings and payroll tax filings.

Many states require businesses to file state tax returns. The kind of return an S Corporation must file depends on the state in which the business is registered. Be sure to familiarize yourself with your state’s particular S Corp tax requirements and tax filing deadlines.

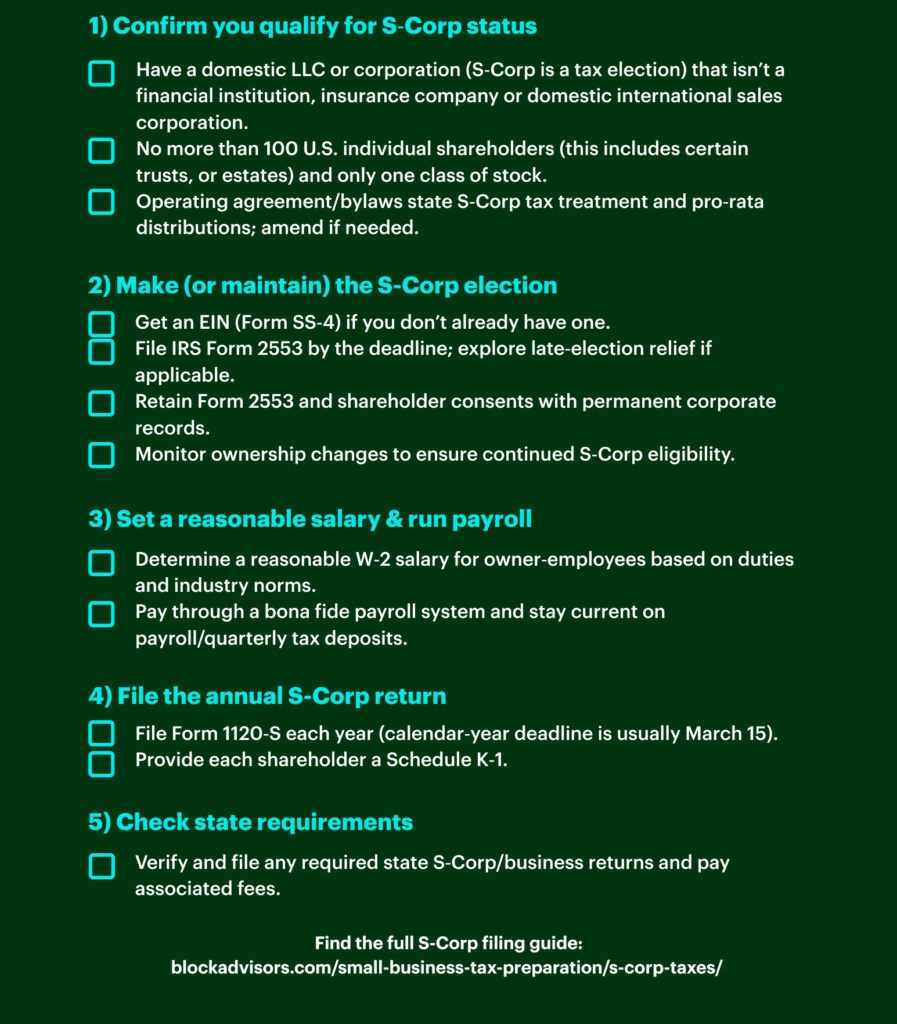

S Corp Tax Filing Checklist

Save or print the S Corp checklist below for a handy guide to some important things to remember if you have recently elected S Corp taxation status or are seeking to maintain it going forward. First, confirm your organization is eligible to file as an S corp. Then obtain an EIN and use the proper forms, such as Form 2553, to make the election. After that, set a reasonable salary to pay yourself and any other owner-employees. And finally, ensure you file your annual federal return (Form 1120-S) on-time and adhere to any state-specific regulations you may be subject to.

Block Advisors is here to help with filing S Corporation taxes

Ready to complete your S Corp filing? Block Advisors can help. Whether you’re starting from scratch or already have an entity, Block Advisors’ business formation tool can make the process easy—simply select “LLC+S Corp”. You can also call the Block Advisors Business Formation hotline at 877-472-1095 to get started.

If you’re still evaluating your options, schedule time with a Block Advisors small business certified tax pro. A Block Advisors expert can help you learn more about how changing your business structure may impact your tax situation. Already have an S Corp? Schedule a meeting with a tax pro to confirm you’re checking off all of the S Corp tax requirements. We can ensure you get every tax credit and deduction you qualify for.

This article is for informational purposes only. The content may not constitute the most up-to-date information and should not be construed as legal advice.