5 min read

March 14, 2023

Block Advisors

Silicon Valley Bank Failure: What to Know for Your Small Business

5 min read

March 14, 2023 • Block Advisors

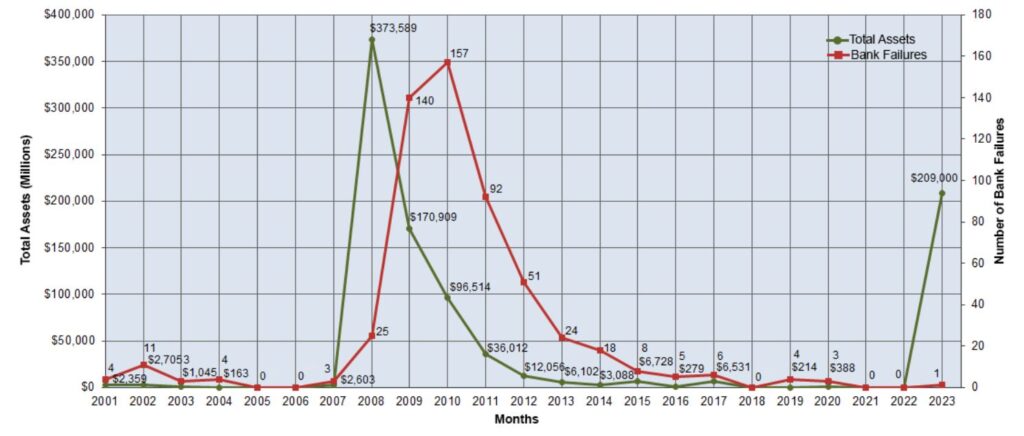

As you may have heard, Silicon Valley Bank – one of the 20 largest banks in the U.S. – failed last week. This event represents the second largest bank failure in U.S. history after the collapse of Washington Mutual during the throes of the 2008 financial crisis.

The headlines in the news are causing some consumers, many of which may be owners of small businesses, to wonder – is my money safe? Keep reading to learn more about this urgent topic and how it could impact you as an entrepreneur, small business owner, or startup partner.

Was Block Advisors, a part of H&R Block, exposed to this event? Is there any risk of being impacted as a Block Advisors client?

No, neither Block Advisors nor H&R Block were exposed to Silicon Valley Bank. As of today, clients have no known risk of interruption to their Block Advisors products and services.

I heard Silicon Valley Bank had many startup clients – how are they being impacted?

As has been widely reported, the Federal Deposit Insurance Corporation (FDIC) has been given special exception by the U.S. government to provide full protection to all Silicon Valley Bank depositors – that is, all client deposits are fully insured. Client funds were available once more starting Monday, March 13, 2023.

According to a Treasury Dept statement, there are SVB stakeholders who are not protected by Silicon Valley Bank’s FDIC insurance. Shareholders and certain unsecured debtholders do not benefit from the same protections as regular depositors. In addition, senior management at SVB has been removed.

The FDIC’s decision to fully cover SVB depositors is a rare departure from normal procedure. Read more about typical deposit insurance limits below.

What is the FDIC? What exactly does FDIC insurance cover?

FDIC stands for The Federal Deposit Insurance Corporation. The group was created after the Great Depression to provide stability to the American banking system and protect consumers from bank failures. Learn more and read FAQs about the FDIC.

A key provision for small businesses is that FDIC insurance covers $250,000 of each customer’s deposits at member institutions. In the exceptional case of Silicon Valley Bank, the US government agreed to remove the $250,000 limit and cover all losses for depositors, though not for shareholders or unsecured debtholders. This situation is still in development.

It is important to note that taxpayers aren’t on the hook for the losses associated with the resolution of Silicon Valley Bank customers. The money paid out to depositors is from loans from the newly funded Bank Term Funding Program through the Federal Reserve.

How do I know if I’ve been exposed to any risk due to the Silicon Valley Bank event?

Silicon Valley Bank’s client niche focused on venture capitalists, startups, and technology companies. In 2021, the institution claimed to back more than half of the venture-backed startups in the entire U.S. For the most part, we’re not talking about local mom-and-pop establishments or creative solopreneur here.

One impact that an average small business owner might feel is with vendors. Even if you don’t have any money directly tied up with SVB, if one of your vendors does, it may interrupt or delay the products and services you receive from them.

While it’s true that the failure of Silicon Valley Bank may have far-reaching impacts, the Treasury Department is working diligently to contain the ripple effect of its closure.

Why do bank failures occur? How are small businesses protected?

Bank failures occur for a variety of complex financial and economic reasons. What’s more, bank closures aren’t particularly rare. According to the FDIC and Brookings, the longest recorded stretch without a bank failure was 2004-2007.

Should a bank fail, its depositors, including small businesses and their owners, are generally covered up to a point – if the bank has FDIC insurance.

What do I need to do to keep my small business safe from future bank failures?

First, make sure your bank has FDIC insurance. This is the easiest way to add a layer of safety to your business funds. Remember – each non-investment account at these banks is covered up to at least $250,000 per accountholder. As long as the small business doesn’t exceed the FDIC insurance limits, it will likely be covered.

For companies with larger banking needs, they can work with several FDIC-insured institutions – as long as each account is “engaged in an independent activity.” This means each account has a defined purpose beyond simply increasing insurance coverage. For example, a company may use one bank with FDIC insurance for their employee payroll and another for their cash reserves. Each account would likely have $250,000 coverage through FDIC insurance.

Finally, it’s a good idea to investigate the financial stability of any institution you do business with. Check the headlines and industry news to make sure you can trust the bank you place your small business deposits with.

How can I ensure the overall financial health of my small business?

Bank failures, like what happened to SVB, pose a real threat to small businesses. However, by taking a few smart actions you can mitigate this risk and look out for the best interests of your company.

Another smart move to ensure the financial health of your company is to keep your small business records in order. Block Advisors has products and services to help small business owners stay on top of their taxes, bookkeeping, payroll, and business formation needs.

Reach out to a Block Advisors small business certified expert today to learn more.