A small business owner’s guide to understanding payroll deductions

Small business owners who add employees will also gain additional financial tasks — including taking care of payroll deductions. What counts as a payroll deduction can vary from employer to employer, but essentially, payroll deductions cover the money taken from your or your employees’ paychecks for a variety of reasons.

There’s a lot to get right where payroll deductions are concerned, especially because of the Internal Revenue Service (IRS) tax rules involved. Thankfully, you don’t have to tackle this task alone.

This guide will walk you through what small businesses need to know about pre-tax deductions and post-tax deductions and which ones count as payroll tax deductions.

Keep in mind: payroll can be time-consuming, but help is available. Whether you need to fully outsource payroll, or just need help with certain tasks, Block Advisors payroll services are here to help you get back to the business you love.

Payroll services made simple

Cross paychecks off your small business to-do list

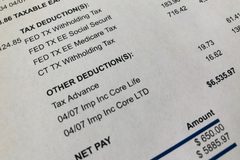

What is a payroll deduction plan?

Before we dive into pre-tax vs post-tax deductions, what exactly is a payroll deduction, and what are some examples of payroll deductions? A payroll deduction plan refers to when an employer withholds money from employee paychecks. This is done for a variety of purposes, but most commonly to take advantage of employee benefits.

A payroll deduction plan can include voluntary deductions and involuntary, or mandatory, deductions. We’ll cover the different types of deductions in more detail below, but common examples of mandatory deductions are 1) when the law requires an employer to withhold money for federal, state, and local income tax and for Social Security and Medicare and 2) wage garnishments. Like it sounds, voluntary payroll deductions are ones that employees give permission for an employer to withhold. Commonly, these are withheld for a retirement savings plan, healthcare, or life insurance premiums.

Pre-tax deductions

Pre-tax deductions are amounts taken from an employee’s pay before taxes are withheld. Taking deductions before taxes lowers an employee’s taxable income, which can save them money come Tax Day. For example, if an employee’s gross pay is $600 a week and they have $100 in pre-tax deductions, they would only pay income tax on $500 per week.

Pre-tax deductions tend to be related to tax-advantaged employee benefits programs.

Common examples include:

- Health insurance premiums

- Retirement plan contributions [E.g., traditional 401(k), SIMPLE IRAs]

- Health savings accounts (HSAs)

- Dependent care accounts.

How pre-tax deductions impact payroll tax deductions

As an employer, knowing what deductions are pre-tax vs. post tax is critical in getting your payroll tax deductions right. Because of the reduction of your employee’s taxable income, pre-tax deductions also effectively reduce your employee’s corresponding payroll tax deductions — i.e., taxes withheld from the employee’s pay.

Those deductions include:

- FICA: Federal Insurance Contributions, which includes Social Security and Medicare

- Federal income tax (FIT taxes)

- State income tax

Pre-tax deductions generally reduce the employer’s share of FICA as well.

Note: Pre-tax retirement plan contributions do not reduce income subject to FICA. Using the same example, if an employee’s gross pay is $600 and the employee makes a $100 pre-tax 401(k) contribution, the employee’s federal and state income tax would be based on $500, but the employee would still pay FICA on $600. The employer’s share of FICA tax would also be paid on $600.

Additionally, pre-tax deductions could reduce what you pay in FUTA taxes for some employees. You pay FUTA on the first $7,000 of wages per employee year.

Post-tax deductions

There are other times you may need to withhold a portion of your employee’s pay. However, these payroll deductions don’t reduce taxable income, so they fall in the category of post-tax deductions, AKA after-tax deductions.

Hence, as the term implies, post-tax deductions are deductions taken from an employee’s pay after taxes are calculated and withheld. These may include:

- Roth 401(k) contributions

- Employee stock purchase plan (ESPP) contributions

- Garnishments for child support or other reasons

- Alimony

- Legally required restitution

- Union dues

How to calculate payroll deductions

Factoring in payroll deductions is a part of the overall calculation of payroll, a task that you’ll run each pay period. To understand that full picture, check out our post on payroll taxes.

For a quick overview of where pre-tax and post-tax deductions fall in that process, review the steps below.

- Calculate employee’s gross pay (hours worked times hourly rate or salary amount).

- Subtract pre-tax deductions.

- Calculate and subtract FICA, FIT, state, and local taxes on the remaining pay subject to these taxes (keeping in mind that 401(k) and other retirement plan deductions are still subject to FICA).

- Subtract post-tax deductions.

Get small business payroll tax deductions help

Calculating payroll and accounting for payroll deductions can quickly eat up several hours every pay period — hours you could spend growing your business. Block Advisors can take care of everything for you so you can get back to what matters most — growing your small business.

See how we can help with your payroll needs and answer your payroll deduction questions.

Schedule a free payroll consultation today.

P.S. We can also help you with other small business tax tasks, like determining when small business taxes are due, complex small business tax forms, and more.

This article is for informational purposes only. The content may not constitute the most up-to-date information and should not be construed as legal advice.